India's small and medium businesses (SMBs) face a billion-dollar problem: commercial insurance is either too expensive, too complex, or simply unavailable. With 75 million registered SMBs in India (Udyam portal), the addressable market for commercial insurance distribution is massive — yet penetration remains under 8%.

This gap represents both a societal need and a massive commercial opportunity. AI-powered insurance distribution platforms can:1) Simplify policy selection through conversational AI agents2) Enable usage-based pricing for seasonal businesses3) Bundle micro-policies for specific risks4) Automate claims processing and reduce fraud

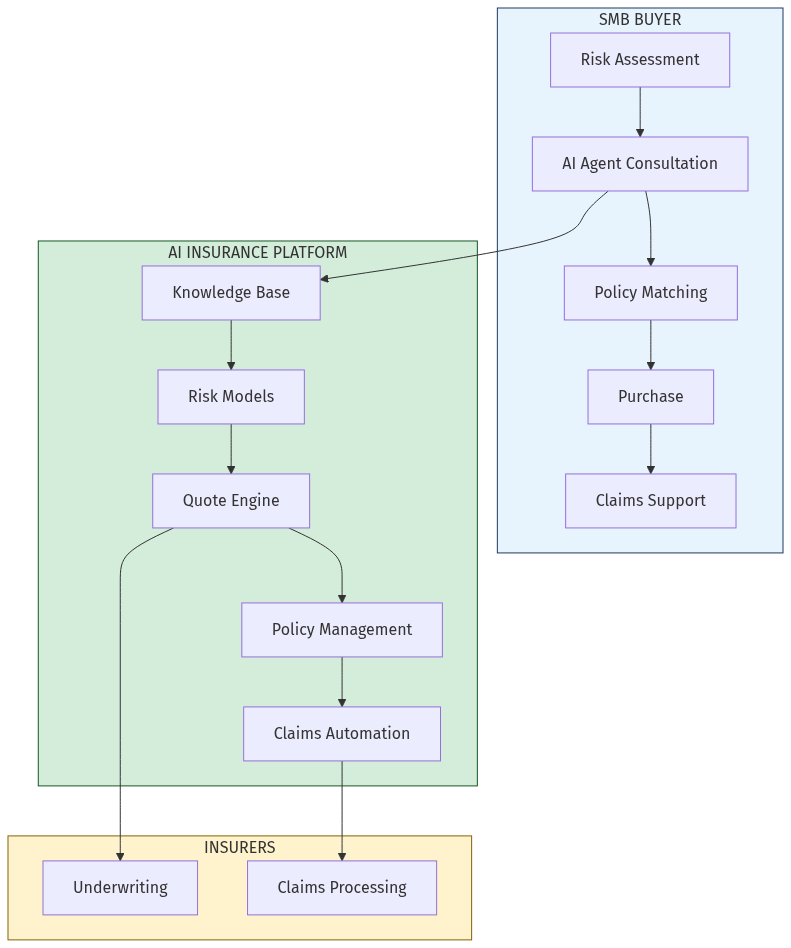

The opportunity: Build an AI-native insurance distribution platform targeting Indian SMBs, starting with specific verticals (retail shops, restaurants, logistics, healthcare clinics) and expanding horizontally.