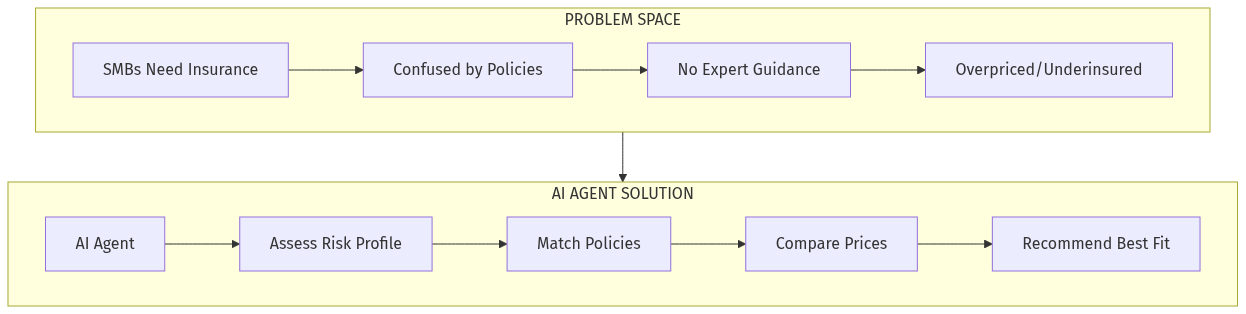

Zeroth Principles: What Is Insurance Really?

The fundamental question: Insurance is a risk transfer mechanism. You pay a premium to protect against uncertain future losses. But the Indian SMB sees insurance differently:

- "It's a scam" — they've heard horror stories of claim rejections

- "It's too expensive" — they see premiums as pure cost, not protection

- "It's too complicated" — they can't parse coverage vs. exclusions

- "I don't need it" — they underestimate their actual risk exposure

The Distribution Gap

Traditional insurance distribution in India operates through:

| Individual Agents | 80% of retail | Fragmented, low expertise, commission-driven |

| Corporate Brokers | Mid-to-large enterprises | Minimum premium ₹5L+, ignore SMBs |

| Direct (Insurer websites) | Tech-savvy segment | Complex UX, no guidance, one-size-fits-all |

| Digital Platforms (Policybazaar, etc.) | Mostly retail | Consumer-focused, limited B2B expertise |

No channel serves the 58 million SMBs that need commercial insurance but can't access human brokers or afford corporate rates.

Who Experiences This Pain?

1. Manufacturing SMEs — Factory insurance, worker's comp, equipment breakdown. Risky, regulated, expensive. Most operate without adequate coverage.

2. Restaurants & Hotels — Fire, liability, business interruption. High claim frequency, high premiums, lots of exclusions. Owners give up and self-insure.

3. Logistics Fleet Owners — Vehicle insurance, cargo insurance, driver coverage. Fleets of 5-50 trucks are invisible to brokers.

4. Healthcare Clinics — Professional liability, equipment insurance, premises liability. Regulatory requirements they don't understand.

5. Retail Shops — Fire, theft, stock insurance. The most "insurable" but most underserved segment.

Incentive Mapping: Why Status Quo Persists

Who profits from the current system?

| Insurance Companies | High margins on under-served segments | No incentive to serve small tickets |

| Individual Agents | Commission on every sale | Focus on high-premium products |

| Corporate Brokers | Volume from large accounts | SMBs are not worth the effort |

| Aggregators | Lead generation fees | Focus on retail, not commercial |

Low coverage → high premiums → low demand → low investment in distribution → low coverage.